Data center valuation requires a holistic view of enterprise value, incorporating both tangible and intangible components across the operating platform.

Unlike conventional commercial real estate, data center value is not derived from land and building alone. It reflects the interaction of physical infrastructure, capital recovery mechanics, operational capabilities, and intangible enterprise attributes that together determine survivability and economic return.

Alpha Consulting US evaluates data center value across these layers, recognizing that enterprise value, asset value, and tax basis recovery are related but distinct concepts.

Tangible Asset Components

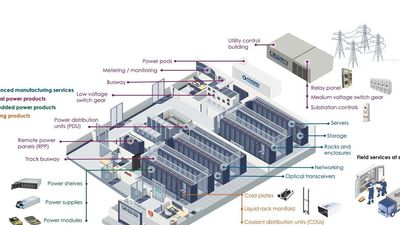

From a tangible asset perspective, data centers are capital-intensive facilities characterized by:

- high-density power distribution and redundancy systems

- mechanical and thermal management infrastructure

- structural and site-specific improvements

- specialized interior build-outs and support systems

These assets form the physical foundation of the enterprise and directly affect replacement cost, capital intensity, and barriers to entry.

Intangible and Enterprise-Level Components

In addition to physical assets, enterprise value reflects intangible and operating elements, including:

- network connectivity and ecosystem positioning

- customer contracts and churn characteristics

- operational scale and reliability reputation

- organizational capabilities and execution risk

These elements do not depreciate for tax purposes, but they materially influence enterprise valuation, risk assessment, and expected returns.

Capital Recovery and Cost Segregation as an Essential Consideration

While cost segregation does not create enterprise value, it is essential to consider within a data center valuation framework because it directly affects capital recovery timing.

Accelerated recovery of capital investment through depreciation classification may influence:

- early-period cash flows

- debt service coverage during ramp-up

- refinancing and recapitalization flexibility

- sponsor-level capital efficiency

Accordingly, cost segregation is evaluated as a critical capital-timing variable, alongside financing structure and operating assumptions, rather than as a standalone tax exercise.

For context, data center projects typically include a combination of:

- §1245 property (often 5-, 7-, and 15-year recovery lives, potentially eligible for bonus depreciation where applicable)

- §1250 property (39-year straight-line depreciation)

- non-depreciable land

Understanding how these components interact is essential for accurate cash-flow modeling and capital-stage analysis.

Land Abstraction and Residual Value Logic

Land value plays a foundational role in separating depreciable and non-depreciable capital.

For data centers, land value cannot be inferred from construction cost or percentage allocation. Improper land abstraction can distort:

- depreciable basis assumptions

- residual value conclusions

- downside and stress-case valuation outcomes

Within our valuation framework, land value is treated as a residual market conclusion, informed by replacement cost logic, depreciation effects, and market evidence consistent with appraisal principles.

Scope Separation and Execution Discipline

Alpha Consulting US does not perform cost segregation studies as part of valuation engagements.

When depreciation classification analysis is required for tax execution, it is treated as a separate execution discipline, coordinated outside the valuation engagement framework. This separation preserves:

- valuation independence

- audit and reporting integrity

- clarity between valuation conclusions and tax implementation

Role Within the Data Center Valuation Framework

Cost segregation considerations are incorporated only to the extent they affect:

- projected cash-flow timing

- capital structure stress testing

- valuation scenarios across development, stabilization, and operation

They inform valuation analysis but do not determine enterprise value.

Execution of cost segregation studies, when required, is delivered through a specialized platform. https://costsegregationexpert.com/