Economic obsolescence represents a reduction in the economic contribution of tangible assets caused by external market conditions, technological shifts, or structural changes in the sources of enterprise value.

In purchase price allocation analysis, tangible asset valuation must remain economically consistent with the overall income-generating capacity of the acquired business. When a substantial portion of enterprise value is attributed to identifiable intangible assets, the remaining economic contribution of the tangible asset base may indicate the presence of economic obsolescence.

Key Analytical Principle

In purchase price allocation analysis, the valuation of tangible assets using the cost approach must remain economically consistent with the income-generating capacity of the enterprise.

When identifiable intangible assets represent a significant portion of enterprise value, the economic contribution attributable to tangible assets may be lower than their replacement cost would otherwise suggest. Under such circumstances, adjustments may be required to reflect the reduced economic utility of the tangible asset base.

Economic obsolescence may therefore arise not only from external market conditions, but also from the relative contribution of intangible assets to the enterprise’s overall economic performance.

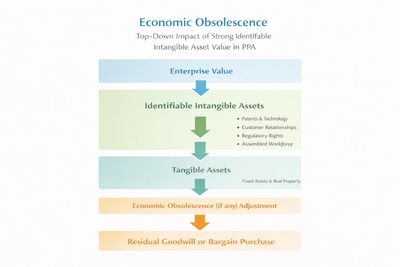

Sequential Allocation Framework

Purchase price allocation typically follows a top-down analytical structure:

- Enterprise Value of the Acquired Business

- Allocation to Identifiable Intangible Assets

- Allocation to Tangible Assets

- Economic Obsolescence (if any) Adjustment

- Residual Goodwill or Bargain Purchase Gain

When identifiable intangible assets consume a large portion of enterprise value, the economic contribution attributable to tangible assets may be smaller than their physical replacement cost.

In such situations, economic obsolescence may be recognized to reconcile the cost approach result with the enterprise’s economic reality.

Relationship Between Intangible Assets and Tangible Asset Value

The economic performance of many modern businesses is driven primarily by intangible assets such as:

• proprietary technologies

• contractual rights and long-term agreements

• customer relationships

• regulatory approvals or operating licenses

• specialized operational systems

• organizational capabilities

When these elements represent the primary drivers of enterprise value, the tangible asset base may contribute less economic value than its replacement cost would otherwise imply.

This dynamic may result in economic obsolescence adjustments within the cost approach valuation of tangible assets.

Impact on Goodwill or Bargain Purchase

Recognition of economic obsolescence may influence the residual allocation of enterprise value.

If the cost approach initially produces tangible asset values that exceed their economic contribution, the recognition of economic obsolescence may:

• reduce the value attributed to tangible assets

• increase the relative significance of identifiable intangible assets

• influence the level of residual goodwill

Conversely, if the aggregate fair value of identifiable assets exceeds the transaction price, the allocation process may result in a bargain purchase gain.

Because of this interaction, economic obsolescence analysis contributes to the internal consistency of the entire purchase price allocation.

Sources of Economic Obsolescence

Economic obsolescence typically arises from external or structural factors affecting the productivity of physical assets.

Examples may include:

• technological advancements reducing competitiveness of existing facilities

• shifts in market demand affecting capacity utilization

• regulatory changes affecting asset operations

• industry restructuring or technological disruption

• modernization requirements for infrastructure assets

These conditions may reduce the economic value contributed by the tangible asset base relative to its replacement cost.

Infrastructure and Technology Industries

The interaction between intangible asset value and economic obsolescence frequently appears in industries involving capital-intensive infrastructure and technology platforms, including:

• digital infrastructure and data centers

• power generation and energy infrastructure

• semiconductor and advanced manufacturing facilities

• telecommunications networks

• automated industrial production systems

In these sectors, enterprise value is often driven by technology platforms, contractual structures, regulatory positioning, and operational expertise, rather than physical assets alone.

Cost Approach Considerations

When applying the cost approach to tangible asset valuation, the analyst must evaluate whether replacement cost accurately reflects the economic contribution of the asset to the enterprise.

If enterprise value is largely driven by intangible assets, the tangible asset base may require economic obsolescence adjustments to ensure that valuation conclusions remain consistent with the business’s actual economic performance.

Failure to recognize such adjustments may lead to overstatement of tangible asset values.

Relationship to PPA Intangible Analysis

Economic obsolescence analysis is closely related to the identification and valuation of intangible assets in purchase price allocation.

When significant enterprise value is attributed to:

• technology platforms

• contractual rights

• regulatory positioning

• customer relationships

• operational systems

• organizational capital

the tangible asset base may represent a smaller portion of the overall enterprise value.

Understanding this interaction helps ensure that the final purchase price allocation remains economically coherent and defensible under audit review.

Closing

Economic obsolescence analysis helps ensure that tangible asset valuation reflects the actual economic contribution of physical assets within the broader enterprise value framework.

Careful consideration of economic obsolescence is therefore essential in purchase price allocation assignments involving technology-driven businesses, infrastructure platforms, and capital-intensive industries.