Purchase price allocation analyses frequently involve complex issues related to the identification and valuation of intangible assets under U.S. financial reporting standards.

While tangible asset valuation is often relatively straightforward, the classification and measurement of intangible assets can introduce significant technical judgment and audit sensitivity.

Improper classification or unsupported valuation assumptions may result in financial reporting adjustments, audit challenges, or regulatory scrutiny.

Alpha Consulting US evaluates these technical dimensions to help ensure that purchase price allocation conclusions remain defensible under ASC 805 business combination accounting and ASC 820 fair value measurement requirements.

Identification of Intangible Assets

Operating businesses frequently contain identifiable intangible assets that must be evaluated separately from tangible assets and goodwill.

Examples may include:

• trade names and brands

• customer relationships

• contractual rights and agreements

• operating licenses and regulatory permits

• proprietary technologies

• software platforms and digital systems

• assembled workforce considerations

• going-concern value

• residual goodwill

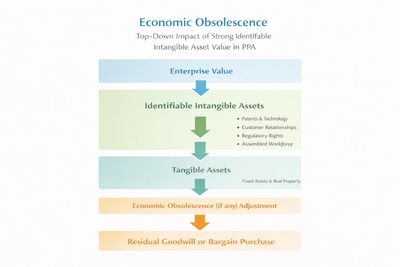

Proper identification of these assets is essential to avoid misallocation of enterprise value between identifiable assets and goodwill.

Accounting for Technology and IPR&D

Acquisitions involving technology development frequently require evaluation of In-Process Research and Development (IPR&D) under ASC 805.

Key accounting considerations include:

• IPR&D must be measured at fair value at the acquisition date

• the asset is recorded as an intangible asset

• the asset is not amortized until the project is completed or abandoned

• subsequent research and development costs are expensed as incurred

Technology-related acquisitions therefore require careful evaluation of development stage, commercialization probability, and expected economic contribution.

Customer Relationship Assets and Attrition

Customer relationships often represent a significant portion of enterprise value in operating businesses.

Valuation of these assets typically requires modeling customer attrition and retention behavior, which may involve:

• historical customer churn analysis

• revenue concentration patterns

• contract duration or renewal expectations

• industry-specific lifecycle behavior

Attrition assumptions directly affect the economic life and valuation of customer relationship assets.

Enabling Assets

Certain assets may function as enabling assets, supporting the generation of value in other intangible assets.

Examples may include:

• regulatory approvals

• operating licenses

• proprietary systems

• technology platforms

• network management systems

• specialized operational processes

Careful analysis is required to ensure that enabling assets are properly recognized without double counting economic value across multiple asset categories.

Covenants Not to Compete

Some transactions include non-compete agreements that restrict sellers from competing with the acquired business.

Valuation considerations typically include:

• enforceability of the covenant

• geographic scope

• duration of restriction

• expected economic impact on the business

In many cases the Differential Value Method is applied to estimate the economic value of these agreements.

Differential Value Method

The Differential Value Method compares the value of the business:

• with the restrictive covenant in place, and

• without the restriction

The difference between these scenarios represents the economic value attributable to the covenant.

This method is frequently used when evaluating restrictive agreements associated with business acquisitions.

Contingencies and Other Technical Issues

Certain acquisitions may involve contingent factors that influence intangible asset valuation.

Examples may include:

• contingent consideration arrangements

• technology commercialization uncertainty

• regulatory approval contingencies

• contractual renewal risks

These factors must be evaluated within the fair value measurement framework of ASC 820.

Strategic Infrastructure and Cross-Border Investment Considerations

In acquisitions involving strategic infrastructure, advanced manufacturing, and enabling technologies, identifiable intangible assets may represent a substantial portion of enterprise value.

This situation frequently arises in cross-border investments, including transactions involving international investors acquiring U.S. infrastructure platforms or technology-enabled enterprises.

Industries where significant intangible asset value may arise include:

• digital infrastructure and data center platforms

• power generation and energy infrastructure

• semiconductor and electronics manufacturing

• battery and energy storage technologies

• industrial automation and robotics platforms

• telecommunications and network infrastructure

In these sectors, enterprise value is often driven not only by physical assets but also by technology capabilities, contractual positioning, and operational systems.

Enabling Technologies and Infrastructure Platforms

Strategic infrastructure businesses frequently rely on enabling technologies that support the performance and scalability of underlying assets.

Examples may include:

• proprietary software systems

• industrial process technologies

• network management platforms

• energy monitoring and control systems

• specialized manufacturing technologies

These enabling technologies may constitute identifiable intangible assets requiring evaluation under ASC 805 purchase price allocation analysis.

Workforce-in-Place and Organizational Capital

In certain acquisitions, the acquired business may possess significant value associated with its assembled workforce and organizational capabilities.

These capabilities may include:

• specialized engineering teams

• experienced operational personnel

• institutional technical knowledge

• integrated operational systems

• proprietary operational procedures

Although assembled workforce itself is generally not recognized as a separate amortizable intangible asset under ASC 805, the existence of an established workforce may contribute to the value of other identifiable intangible assets.

Role in Infrastructure and Technology Businesses

Workforce-related capabilities are particularly important in industries involving complex infrastructure operations or advanced technology platforms, including:

• data center operations

• semiconductor fabrication

• advanced energy infrastructure

• industrial automation and robotics

• high-precision manufacturing

In these sectors, operational performance often depends heavily on technical expertise and coordinated organizational capabilities.

Importance of Defensible Valuation

Purchase price allocation analyses are frequently reviewed by:

• external auditors

• internal accounting teams

• financial reporting regulators

Accordingly, intangible asset valuation requires:

• disciplined identification of assets

• transparent valuation methodologies

• reasonable economic assumptions

• clear documentation supporting conclusions

A defensible analytical framework helps ensure that PPA conclusions remain robust under audit review and financial reporting scrutiny.

Closing

Intangible assets often represent a substantial portion of enterprise value in modern acquisitions.

Careful identification, classification, and valuation of these assets is therefore essential to ensure that purchase price allocation results remain consistent with accounting standards and defensible under audit review.