In purchase price allocation assignments, tangible operating assets are frequently valued using the cost approach, particularly when active secondary markets for comparable assets are limited.

In this context, analysts must evaluate multiple forms of depreciation affecting the economic utility of the acquired assets.

Two key categories are physical deterioration and functional obsolescence, both of which arise from characteristics of the asset itself.

These factors differ from economic obsolescence, which arises from external market conditions or shifts in enterprise value drivers.

In the PPA framework, these adjustments are applied to tangible operating assets such as industrial facilities, infrastructure systems, and specialized equipment, rather than to traditional real estate appraisal contexts.

Physical Deterioration

Physical deterioration represents the loss of value caused by aging, wear, and physical condition of the asset.

In PPA assignments this analysis often applies to assets such as:

• industrial machinery and manufacturing equipment

• infrastructure systems

• power generation equipment

• telecommunications systems

• specialized production facilities

Physical deterioration may be evaluated through:

• effective age and remaining life analysis

• engineering condition assessment

• maintenance and replacement history

• expected remaining service life

These considerations help determine the remaining economic usefulness of the asset within the acquired enterprise.

Functional Obsolescence

Functional obsolescence occurs when an asset becomes less efficient or less useful due to design limitations, technological change, or operational inefficiencies.

Unlike physical deterioration, functional obsolescence may occur even when the asset remains in good physical condition.

Examples may include:

• outdated production equipment or industrial processes

• inefficient plant layout

• excess operating costs relative to modern facilities

• capacity mismatches compared with current production needs

Functional obsolescence may be curable or incurable, depending on whether the deficiency can be economically corrected.

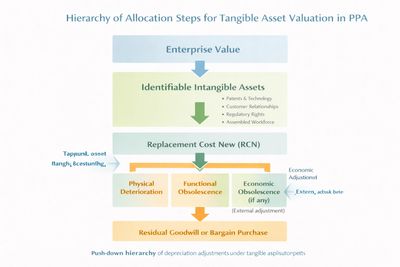

Push-Down Hierarchy of Depreciation Adjustments

In the tangible asset portion of purchase price allocation, depreciation adjustments follow a specific push-down hierarchy.

This structure helps avoid double-counting of value loss and ensures that each form of depreciation is applied to the appropriate remaining value base.

Standard Sequence of Adjustments

Replacement Cost New (RCN)

The analysis begins with Replacement Cost New, representing the cost to construct or acquire a modern asset providing equivalent utility.

This reflects the cost of a facility designed according to current engineering and technological standards.

Less: Physical Deterioration

The first adjustment removes value lost through wear, aging, and physical consumption of the asset.

Because this represents the consumption of the asset’s physical life, it is applied first in the sequence.

Less: Functional Obsolescence

The second adjustment addresses internal inefficiencies or design limitations relative to modern technology or operating standards.

Functional obsolescence is applied to the value remaining after physical deterioration has been removed.

Less: Economic Obsolescence (if any) Adjustment

The final adjustment addresses external economic factors affecting the asset’s value.

This adjustment is applied to the remaining value after both physical deterioration and functional obsolescence have been recognized.

The remaining base is often referred to as:

Replacement Cost New Less Depreciation and Functional Obsolescence (RCNLDF).

Applying economic obsolescence at this stage ensures that external market conditions are measured against the true remaining economic value of the asset.

Avoiding Misattribution of Value Loss

Applying the adjustments in the correct sequence is important to avoid misattributing value loss.

For example, if economic obsolescence is measured using an income shortfall method before functional inefficiencies have been addressed, the analyst may incorrectly attribute internal operational deficiencies to external market conditions.

The push-down hierarchy ensures that:

• internal asset deficiencies are addressed first

• external market conditions are applied only to the remaining value

• double counting of depreciation is avoided

Inutility in Large Infrastructure Assets

In large infrastructure assets such as power plants, refineries, and industrial facilities, economic obsolescence often manifests as inutility.

Inutility occurs when an asset is physically capable of production but market demand no longer supports its full operating capacity.

Examples may include:

• excess generation capacity in energy markets

• reduced industrial output demand

• technological displacement of legacy systems

Applying economic obsolescence last ensures that market effects are not incorrectly applied to portions of value that were already reduced through physical deterioration or functional obsolescence.

Relationship to Intangible Asset Value

In modern infrastructure and technology businesses, enterprise value may be driven significantly by identifiable intangible assets such as technology platforms, contractual rights, and operational systems.

When these elements represent major value drivers, the tangible asset base may contribute less economic value than its replacement cost suggests, which may interact with economic obsolescence considerations.

This relationship is further discussed in the Economic Obsolescence section of this website.

Closing

Physical deterioration and functional obsolescence represent important components of depreciation analysis in tangible asset valuation for purchase price allocation.

Applying these adjustments in a structured sequence helps ensure that the cost approach reflects the actual economic utility of the tangible assets within the enterprise.

This analytical discipline is particularly important in acquisitions involving capital-intensive infrastructure, advanced industrial systems, and technology-driven businesses.